An Incomplete End of Year Recap

My hopes for a more thorough recap of the state of the lidar sector have again been thwarted by work, life, limited time, and the self-imposed feeling of being rushed after the most recent 8-K filings, I must post before the big one, I need something to look back on: "Wow I had it all right" or "Wow how I had it all wrong."

Let's begin.

AEye

- 9/15/2023 - 8-K filed due to Wen H Hsieh resigning from Board of Directors and triggering non-compliance with NASDAQ (audit committee must consist of at least three members) source

- 10/30/2023 - 8-K filed Jonathon Husby appointed as class III director source

- 10/31/2023 - 8-K filed Luis Dussan's employmeent as CTO terminated (original founder), remains as board director source

- 11/6/2023 - 8-K filed, business focus shifting from industrial markets to automotive, thus recording ~$5M write-down on inventory related to industrial, and ~$2M cash charge related to workforce reduction (29 positions to be cut in Q4 2023) source

- 11/7/2023 - 8-K filed, retention agreement for General Counsel Andrew Hughes and CFO Conor Tierney, stick around until Dec 2024, GC gets $385k, CFO $330k source

- 11/9/2023 8-K filed, financial results for Q3 released: $200k revenue, net loss -$17M, $46M cash on balance sheet source

- 12/13/2023 8-K filed, shareholders vote for reverse stock split (PPS at time $0.10-0.13) source

12/18/2023 8-K filed source:

Following the December 4, 2023 announcement by Continental AG (“Continental”) related to its corporatewide restructuring and expense reduction efforts, representatives of Continental informed AEye, Inc. (the “Company”) that Continental intends to discontinue the parties’ joint lidar development program, including any further development of the HRL131 lidar product line. Continental and the Company are currently engaged in negotiations regarding a transition of the joint lidar program.

Having made significant progress in product performance, maturity, and cost reduction over the last six months, the Company intends to address the automotive market interest it continues to see by furthering its ongoing discussions with other Tier 1 automotive suppliers. The Company continues to focus on commercialization of its next generation 4Sight™ Flex product, which is believed to be the only 1550 nanometer high-performance lidar capable of in-cabin integration.

4Sight Flex is their latest compact 1550nm offering designed for behind the windshield integration, 120o horizontal (H) x 30o vertical (V) field of view, angular resolution of up to 0.05° x 0.05°, and long-range detection of up to 275 meters at 10% reflectivity, all at approximately half the size and up to 40% lower power consumption compared to AEye’s first-generation design (HRL131). In addition to smaller footprint the sensor also includes AEye's 4Sight perception software, which is software configurable, update-able via OTA. Whether or not that's seen as an advantage or not to Automotive OEMs remains to be seen, it's hard enough managing their own code, see below, but to validate changing 3rd party code?

Cepton

- 9/7/2023 8-K filed, shareholders vote for reverse stock split, source

- 9/18/2023 8-K filed, 1 for 10 reverse stock split approved by BOD, effective 9/21/2023 source

- 11/9/2023 8-K filed for Q3 financial results source

From Q3 PR 11/12/2023 source:

Jun Pei (CEO):

While Cepton stands ready to meet start-up production volume requirements, our lead OEM customer has experienced some recent automotive industry headwinds that was publicly known which resulted in some vehicle launch delays. We're working through these and are confident our efforts in preparing for the anticipated production volume will be fully appreciated in the near future.

Moving on to the technology. Our software development work has become increasingly important matching our hardware development work with our customers. Through extensive collaboration with our automotive OEM customers, our software teams have developed the best-in-class automotive software validation suite for Ethernet-based sensors. In automotive application where our lidar is a key sensor modality, our domain expertise enables plug-and-play software solutions that can integrate into the broader ADAS stack.

Cepton remains steadfast in pursuing opportunities in automotive industry and remains in a good position to win additional series production award with sourcing decisions on the horizon.

Mitch Hourtienne:

On our RFI and RFQ activity, we remain in the final sourcing discussion for another major OEMs lidar sourcing decision for our long-range lidar, the same as we have reported last quarter. This decision is expected by the end of the year and has been delayed somewhat as a result of macroeconomic headwinds in the automotive industry. We've also entered final sourcing discussions with a major trucking OEM for our short-range lidar with the decision also expected by the end of the year.

We hope to share more details in the upcoming months about production sourcing awards

12/13/2023 8-K filed source:

As previously disclosed, Cepton, Inc. (“Cepton” or the “Company”), alongside its tier 1 partner, Koito Manufacturing Co., Ltd. (“Koito”), were selected as the sole lidar provider to support a significant ADAS program through 2027 (the “series production award”). Following the series production award, Koito has, from time to time, issued purchase orders to the Company for lidar components under the series production award. On December 11, 2023, Koito informed the Company that the original equipment manufacturer that awarded Koito the series production award has decided to re-scope its ADAS product offerings and, as a result, all outstanding purchase orders from Koito to the Company that relate to the series production award have been cancelled. As is customary when an automotive program changes, Cepton plans to seek project investment cost recovery related to any delay or cancellation of an existing program to the extent possible.

Cepton continues to engage with the original equipment manufacturer in defining sensor needs and system architecture for the next generation ADAS offerings. Cepton and Koito’s collaboration on joint product development and go-to-market strategies, and engagement with other global original equipment manufacturers on new system sourcing opportunities, is expected to continue.

12/21/2023 8-K filed source:

SAN JOSE, CA, December 21, 2023 – Cepton, Inc. (“Cepton” or the “Company”) (Nasdaq: CPTN), a Silicon Valley innovator and leader in high performance lidar solutions, announced today that it has received a non-binding indication of interest from Koito Manufacturing Co., Ltd. (“Koito”) to acquire (the “Proposed Transaction”) 100% of the outstanding shares of the Company not already owned by Koito or certain other potential rollover participants including Dr. Jun Pei, Cepton’s President and Chief Executive Officer (collectively, the “Rollover Participants”). Koito has stated in the indication of interest that the terms of any potential agreement between Cepton and Koito would be contingent on certain conditions, including, in particular, satisfactory completion of due diligence review, rollover by the Rollover Participants, retention of key employees, negotiation and agreement of transaction structure and transaction documents, approval of the Proposed Transaction by the board of directors of Koito, and approval by a simple majority vote of the outstanding shares of Cepton.

Cepton’s Board of Directors, through a special committee thereof (the “Special Committee”), will carefully evaluate Koito’s indication of interest within the context of the ongoing review of various alternatives and in consultation with any financial and legal advisors it may retain

No assurance can be given that a definitive transaction with respect to Koito’s indication of interest or any other potential transaction will eventually be consummated. Cepton does not intend to make any further announcements about any of the various alternatives that are being evaluated unless and until Cepton’s Board of Directors and/or the Special Committee has approved a specific transaction or otherwise determines that further disclosure is appropriate or necessary.

Like AEye, Cepton has recently been put through the wringer with losing their contract with GM, however they believe they have a good chance of winning a new deal of substantial size soon, some seem to think Ford. Supply chain stability will surely be on the forefront of discussions with OEMs, will Koito stepping in be enough to secure the deal?

Innoviz

8/14/2023 6-K filed source: public offering

8/16/2023 6-K filed source:

Dear Fellow Shareholders,

Following our successful capital raise last week, I want to offer additional color on the context and strategy behind the follow-on offering and what it accomplishes for our investors.

Innoviz is currently participating in over five active RFQ sourcing processes, all with major automotive OEMs. While our previous cash balance was meaningful and gave us a substantial financial runway, the Board and management team felt that adding additional cash to the balance sheet would give us the best possible odds of securing further customer wins – an important step in the growth of our company. We believe we are in a once-in-a-lifetime market share capture window for the automotive LiDAR industry. We also believe that we have the technology that is needed to be a market leader, and now I am confident that we have the balance sheet that is needed as well.

Oren Buskila, my fellow co-founder and our Chief R&D Officer, and I both invested in last week’s follow-on offering, and Amichai Steimberg, our Chairman of the Board, increased his position in the company this week as well. This reflects our strong belief in the long-term success of the business and our confidence in our ability to execute on the many catalysts that lie ahead of us this year and next. Below I will outline a few key components of the Innoviz story to give you a better sense of our vision for the company and the tremendous opportunities that lie ahead.

| • | Winner Takes Most Market: At Innoviz, we believe the automotive LiDAR industry is ultimately going to be a winner-takes-most market. We expect that early leaders in the LiDAR industry will be able to create high barriers to entry versus new competitors, built upon technology leadership and volume-based cost advantages. Establishing an early leadership position can be an important component to long-term success. |

| • | The Flywheel Effect: In the LiDAR industry, we believe that wins can lead to more wins. |

Securing additional awards in the near-term can further drive our technology leadership, capture additional NRE funding, and enhance volume-based cost advantages, leading to the potential for additional success thereafter.

| • | Significant Market Share Capture Window: On our first quarter earnings call this year I spoke about how several programs with major OEMs transitioned from RFIs to RFQs during the quarter, and with roughly half of our pipeline now in the RFQ phase, we are actively quoting on more than five RFQ’s in parallel. OEMs are planning for these programs now and there are a slew of decisions that I expect to come in 2023-24. Since many of these programs are 8-10 years long, this is an opportunity to capture long-term market share in an industry where growth is poised to move quickly. |

| • | Cash Runway: The cash secured by the recent capital raise extends our financial runway beyond the market share capture window, and if we secure additional awards, we can push our cash runway even further. |

| • | NREs can Unlock Additional Cash Runway: Part of our strategy to become a Tier 1 automotive supplier was predicated on the fact that it is the only way to unlock meaningful non-recurring engineering (NRE) bookings. We have previously disclosed that the typical NRE quote within our RFI/RFQ pipeline is for $20-40 million and we have some above the high end of that range, closer to the $60 million mark. These pre-production income streams represent a cash payment that can meaningfully offset our cash burn. |

| • | Strong Track Record of Execution: In 2022, we hinted at a major new OEM customer and months later we delivered the Volkswagen Group. Coming into this year we hinted at a program expansion, and the next quarter we delivered the light commercial vehicle announcement. In the first quarter of 2023 we said we were working on a Minimum Risk Maneuver (MRM) solution for a customer, and on our second quarter earnings call we announced the BMW B-sample with MRM and our AI compute module. And for the last year, we’ve been pointing to a 2023 start of production (SOP) with the BMW 7 Series, and we began shipping the production units early in the third quarter. We want investors to recognize that we are delivering on the things that we say we are going to do. I am confident that we can continue our track record of executing. |

When combined, these factors point to a strong backdrop for Innoviz in the programs that we are actively competing on. I believe that the incremental capital that we raised will position us more favorably to deliver these wins. Thank you for your continued support and ongoing belief in the Innoviz mission.

Sincerely,

Omer Keilaf

10/24/2023 6-K filed source:

Innoviz Technologies has not experienced any immediate material operational or financial impact following the terrorist attacks in Israel on October 7th or the pursuant conflict thereafter. The Company’s headquarters are based in Rosh Ha’Ayin, in the center of the country, away from the Southern and Northern borders. Furthermore, Innoviz is a global company, with its high-volume manufacturing sites located in the United States and Germany, and a future site planned for Asia. The Company has the ability to locate high-volume manufacturing anywhere a customer desires through its flexible and capital efficient contract manufacturing strategy. The Company continues to monitor its ongoing activities and will make any needed adjustments to ensure the continuity of its business while supporting the safety and well-being of its employees.

Additionally, Innoviz is reiterating its 2023 financial targets, including the ramp in revenue expected in the second half of the year. The Company previously communicated that third quarter revenues are expected to approximately double versus the second quarter of 2023, with an even larger increase expected in the fourth quarter of 2023.

11/8/2023 6-K Q3 financials source, transcript, slides:

Omer (CEO):

In the early weeks of the third quarter, we moved forward on a very important milestone in our company’s history, moving into SOP with our BMW Gen 1 program. The components are shipped to Magna for final assembly at a plant in Michigan and then head to BMW for installation on the 7-Series.

And as I mentioned earlier, we also locked in the final SOP-ready version of our AI-enabled perception software and shipped it on time to BMW as well.

We have been pointing to the back half of 2023 launch for a while, so to get to this phase is a huge win, and I believe we are building a track record of credibility that includes delivering on our goals and timelines.

There are a number of other LIDAR companies out there claiming to compete with us in automotive LIDAR space. But some don’t even have a single series production award yet. And some have awards, but have yet to execute on SOP-related milestones. From our experience, those who haven’t executed on these milestones, don’t even know how much they don’t know at this point.

The other program that we have that is moving into SOP is our Shuttle program. As a reminder, this is a full Level 4 program. The customer is a leading automotive supplier who is building this vehicle directly in order to become an early leader in the rapidly growing autonomous shuttle market.

We expect this program to be a fully driverless electric vehicle capable of carrying over 20 passengers and the ability to operate 24 hours a day. The earliest applications are likely to be people movers in environments like airports, college campuses, private communities, and corporate campuses. But the shuttle is also expected to be capable of operating in mixed traffic and dedicated lanes. This opens it up to urban centers and possibly even suburban environments where it could become a lower cost or much more flexible alternative to legacy public transportation models.

Last quarter we shared that we have begun development of an all-new second generation LiDAR platform that is built around the InnovizTwo sensor and our AI-enabled perception software stack. We also spoke in detail about how we have the potential to meaningfully grow our software content and dollar value, and this quarter I wanted to give you a little bit more color on what the overall change in that content per vehicle could look like.

A key part of our long-term strategy is to drive the price of the LIDAR sensor lower in order to drive adoption rates higher. Tailwinds from potentially rapid increases in volumes as we move up the S-curve have the opportunity to be a meaningfully positive net contributor to both the revenue and profit line.

But as we drive sensor costs lower, our goal is to continue to drive content per vehicle higher by expanding into new product categories. To articulate this point, I think it would be helpful to compare how our business model and CPV has evolved over time.

In the first generation program with BMW we were operating as a Tier 2 supplier, selling only components to Magna – not a full LIDAR to BMW. Magna takes those components, integrates them into other parts of the hardware and then sells the finished LIDAR to BMW. We were only capturing a portion of the total system value – around $600-700 per vehicle.

Since winning that contract in 2018 we have undergone two transformative changes. First, we transitioned from a Tier 2 supplier to a Tier 1, capturing a much larger portion of the economics and moving from selling components to selling full systems. This move also increases the amount of non recurring engineering, or NRE revenues available to us.

The second transition was moving from InnovizOne to the InnovizTwo. Thanks to several technological and engineering breakthroughs, we moved from a design that was built on four lasers and four detectors to a design built on a single laser and single detector. This, along with the host of other changes resulted in a bill of materials, or BOM, that was roughly 70% lower than the InnovizOne.

This was a massive reduction in cost, and these changes were a key catalyst for our Tier 1 design win with Volkswagen in 2022 and the big acceleration in commercial activity we have seen since then.

Next, I wanted to give a quick update on Volkswagen. Overall, our program with VW continues to progress nicely, and the sensor suite for the initial program continues to evolve. We moved from the A sample to the B-sample back in March and we continue to test and fine tune within the B-sample stage, having released our new B2.0 sample during the quarter. Each new version unlocks incremental levels of performance, functionality, and industrialization, and the newest version is based on our second generation custom ASIC. Last quarter we shared with you that we have finished the tape-out of the ASIC. This new chip has two key benefits. The first, is that it unlocks a configuration that enables much more range, taking our maximum detection range from 300 to over 450 meters. And the second is that it can support much higher resolution. The more powerful chip enables us to produce millions of more points. In fact, we were able to nearly double the total number of points that we can process per second. This can power a higher density point cloud with even better resolution than before.

Continuous improvements like this in both our sensor and software suite are aiding our conversations with OEMs. With Volkswagen specifically, we are in advanced conversations exploring the potential addition of multiple platforms that would be incremental to our initial series production award. We hope to have more to share on this in the coming quarters.

But as I always say, video speaks better than words

When we look at the LIDAR industry, we believe our next 1-2 deals have the potential to permanently shape the industry.

There's much to unpack from Innoviz, management seems to be bullish by purchasing additional shares, they expect first mover advantage to keep their foot in the door to continue winning more models and brands across the Automotive OEM's offerings. They reached SOP for InnovizOne for BMW 7 series in Q3, delivered their new AI based perception software to BMW for testing, finished B-sample of InnovizTwo for VW with configurations that offer increased resolution and range (300m -> 450m), exact specifications is admittedly unclear. They also claim to be approaching SOP for a shuttle program for a "leading automotive supplier who is building this vehicle directly in order to become an early leader in the rapidly growing autonomous shuttle market." Total speculation but interestingly ZF has recently killed their autonomous shuttle program source:

it will no longer pursue the goal of facilitating entire autonomous transportation systems, including shuttles and their fleet management; will focus on position as a premium supplier for autonomous driving technology.

Perhaps we'll see another 6-K filed shortly?

Microvision

11/8/2023 8-K filed source:

Sumit Sharma (CEO):

I'm happy to report that we remain on course on our main 2023 objective of securing multiple designs wins with nominations from OEMs. We remain the only LiDAR company that offers multiple technology nodes, with highest resolutions, smallest form factor LiDAR with our MEMS-based long-range MAVIN, as well as small form factor short-range sequential flash-based MOVIA LiDAR product lines. We continue developing our revenue streams from strategic and other channels, and I'm satisfied with the progress so far.

The biggest opportunity for the company remains in strategic partnerships with automotive OEMs for our LiDAR products. Establishing a predictable level of direct sales from non-automotive customers is also very important for all LiDAR companies to be successful. I would like to start by updating you on our progress on multiple opportunities for LiDAR nominations, target launch timelines, and the magnitude of deals we're looking at. Our teams remain engaged with multiple OEMs looking to identify their next LiDAR partner for expanded ADAS safety for their passenger vehicles and commercial trucking product lines to be nominated in 2023, and be ready for start of production as early as 2027. The combined lifetime volume of all the programs up for nomination in 2023 are for millions of units with their cumulative revenues of between $1.2 billion and $950 million over the life of production.

Anubhav Verma (CFO):

As we navigate the final rounds of RFQs with OEMs, customary visits and quality audits at production facilities have been important for customer confidence. In our experience, OEMs want to see multiple manufacturing locations around the globe, including in the EU, Asia and North America. Of course, key points in our RFQ negotiations center on the allocation of liability and product warranties. In terms of operating expenses, including R&D, MicroVision has a meaningful strategic advantage when it comes to quickly and efficiently scaling up operations.

Scaling operations with multiple customer wins will not require us to add proportional headcount to our engineering teams. We do not believe that we will need to add more hardware engineers as we expect to just need more dedicated Project Managers along with quality and operations team to manage multiple relationships as we increase volumes and enjoy the resulting economies of scale. We have the ability to add such resources at OEMs preferred locations in North America and Germany. We see no need to double or triple headcount to support potential revenue growth.

The majority of this third quarter, revenue is related to our MOSAIK software product and is from a leading OEM. We expect continued momentum in revenue in the fourth quarter and expect sequential growth to hit our updated 2023 revenue targets of $6.5 million to $8 million. Now this revenue is slightly below our previously announced range of $10 million to $15 million. The reduction in our revenue expectations is primarily related to direct sales with some revenue opportunities appearing to have moved into 2024.

11/14/2023 8-K filed source:

REDMOND, Wash. – November 14, 2023 – MicroVision, Inc. (Nasdaq: MVIS), a leader in MEMS-based solid-state automotive lidar technology and ADAS solutions, today announced its executive management team and several members of its Board of Directors have entered into private placement agreements to purchase shares of the Company’s common stock. Pursuant to the agreements, the purchasers will acquire an aggregate of approximately $100,000 of MicroVision’s common stock at $1.97 per share, yesterday’s closing price as reported on The Nasdaq Stock Market.

“As the independent Chair of the Board, I have great confidence in MicroVision’s management team and the Company’s business strategy,” stated Mr. Robert Carlile. “I believe MicroVision has a promising future ahead.”

“These share purchases by members of the Board of Directors and the executive team reflect our collective optimism toward accomplishing our strategic and operational goals for MicroVision and our continued commitment to building and achieving long-term value for our stockholders,” said Sumit Sharma, the Company’s Chief Executive Officer. “We thank our stockholders for their support and belief in what we are building here at MicroVision.”

12/4/2023: Microvision joins forces with Luxoft, Dr. Thomas Luce, MicroVision Managing Director and VP Business Development, said: "Teaming up with Luxoft is a great opportunity for MicroVision to accelerate the implementation of our Mosaik validation and ground truth software suite and to boost Luxoft's outstanding capability of providing a highly efficient validation solution." which sounds as though Luxoft will help obtain new customers for Microvision by offering Mosaik to their existing customer base. Additionally mentioned: "This collaboration will go further to advance ADAS and AD applications - Luxoft and MicroVision are also developing a solution to generate a digital twin for an SAE Level 3 highway pilot. Watch this space."

12/14/2023 8-K filed source:

REDMOND, Wash. – Dec. 14, 2023 – MicroVision, Inc. (Nasdaq: MVIS), a leader in MEMS-based solid-state automotive lidar technology and ADAS solutions, today reiterated its 2023 revenue guidance and provided updates on engagement with OEMs.

“As we wrap up a year of strong growth and momentum for MicroVision, we want to give a brief update to shareholders about where we are and where we’re going,” said Sumit Sharma, MicroVision’s Chief Executive Officer. “Consistent with our previous statement, we expect our 2023 revenue to be near the top end of the $6.5 - $8.0 million range. Looking ahead, I am excited about opportunities to ramp revenue from non-automotive markets through our direct sales channel.”

“In addition, on strategic sales, our forward momentum with multiple potential customers continues, but we are pushing out our expectations of nomination timing into the first quarter of 2024. We feel confident in our engagement with OEMs as we are receiving demand for large orders of samples ahead of nomination,” continued Sharma. “Deep discussions continue as we work through the commercial terms of these significant and market-changing partnerships.”

12/21/2023 8-K filed source:

On December 15, 2023, MicroVision GmbH (the “Subsidiary Company”), a wholly-owned subsidiary of MicroVision, Inc., entered into a Lease Agreement Concerning Office Premises (the “Lease”) with Victoria Immo Properties I S.à r.l. (the “Landlord”), pursuant to which the Subsidiary Company will lease approximately 5,500 square meters (or approximately 60,000 square feet) of space located in Hamburg, Germany (the “Premises”) that it will use primarily for general office space and product testing.

The Lease provides for an initial term of five years (the “Term”) commencing on the date the Premises are delivered to the Subsidiary Company, which is expected to occur between August 1, 2024 and December 31, 2024. In connection with the execution of the Lease, the Subsidiary Company will provide the Landlord a security deposit of approximately $1 million.

Pursuant to the Lease, for the first year of the Term the monthly base rent will be approximately $117,000. For each subsequent year, the base rent is subject to an annual market rate adjustment. In addition to the monthly base rent, the Subsidiary Company will pay additional rent comprised of certain operating, management, and ancillary expenses, subject to certain terms and limitations set forth in the Lease, and applicable taxes. The Subsidiary Company has the option to extend the Term for the Premises two times, each for a three-year period.

The Premises are intended to replace the office space currently being rented by the Subsidiary Company upon expiration of the leases associated with those properties. A description of the Subsidiary Company’s existing lease arrangements can be found in MicroVision, Inc.’s Quarterly Report on Form 10-Q filed on November 9, 2023.

The foregoing description of the Lease is a summary, is not complete, and is qualified in its entirety by the terms and conditions of the actual Lease, which will be filed as an exhibit to the Company’s Annual Report on Form 10-K for the year ended December 31, 2023.

Sensor fusion between lidar and radar appears to have been completed: MicroVision - Sensor Fusion Demonstration August 2023 (youtube.com)

Year revenue guidance revised from $10-15M to $6.5-8M due to Movia orders pushed to 2024, in November on track to announcing multiple design wins by end of year, less than thirty days later design win announcement pushed to Q1 2024. Can you say delay, delay, delay? But can you really blame them? Don't share enough information and investors eat you alive, share too much and your words become gospel as though everything is under your control. Cepton expected a design win announcement in Q3/Q4, so far nothing, Innoviz claimed multiple wins in the market would be announced around the end of year, so far nothing, it's all still up for grabs...

Luminar

2/28/23 Luminar Day source:

Luminar AI Engine and Exclusive Scale.ai Partnership: Unleashing the Potential of Luminar’s 3D Lidar Data

Because data is key to unleashing the next generation safety and autonomy capabilities of Luminar sensors, the company invested in software development early on.

Since 2017, Luminar has been quietly developing AI capabilities on its 3D lidar data to further the performance and functionality of next-generation safety and autonomy on vehicles. Today at Luminar Day, the company is showcasing its machine-learning based Luminar AI Engine enabling greater accuracy and precision of detecting objects, vehicles, pedestrians, and beyond. Luminar expects more than a million Luminar-equipped vehicles on the road over the next few years capturing 3D data, which has the opportunity to fuel its AI engine with the most comprehensive, accurate, and up-to-date 3D dataset in the industry. This captured lidar data can also be used for Luminar’s HD Mapping in constructing a 3D model of the driveable world.

Scale.ai, the leader in data infrastructure for artificial intelligence applications, and Luminar are partnering to supercharge the Luminar AI Engine. Scale’s technology will now be available exclusively to Luminar and no longer accessible to other providers of lidar. Scale also will be Luminar’s exclusive provider of data labeling and AI tools. Alexandr Wang, Founder and CEO of Scale, will speak to the partnership on stage with Austin Russell at Luminar Day on today’s livestream.

11/8/2023 8-K source, EC transcript:

Austin Russell (CE):

Mexico facility would support up to 250,000 centers [sensors] or corresponding vehicles per year. So it’s been a great starting point with that. And then, we’ll have ultimately a similar test with TPK and Mercedes and everything down the line as that all plays out accordingly. So yes, we’re excited for the future. And it’s really all systems go with Volvo. It’s going to be a huge game changer as they launch and scale this EX90 next year.

And, you take a look at like the Mercedes program, for example, in the collaboration that we have with them on that, with NVIDIA, that’s something that’s obviously been public. And again, it goes to show what you can do when you combine the respective leading technology companies together to create an incredible solution

Aileen Smith: All right. Our next question is going to be for Tom and that is, is Luminar in danger of bankruptcy?

Tom Fennimore: Aileen, the short answer is no. I understand why some shareholders would ask that question, given the recent stock price performance. But when you actually look at our most recent results for Q3, We cut our non-GAAP gross loss almost in half which puts us on trajectory to get it to positive by the end of the year as those launch-related costs continue to wind down as we successfully industrialize Iris. We cut our free cash spend by nearly $20 million during the quarter which puts us on track to kind of get it into that $35 million to $40 million dollar range for Q4. We had over $320 million of cash and liquidity as a quarter end we’re on track to have over $300 million of cash and liquidity at the end of the year.

So when you kind of look at where we our targets for ending the year we’re going to have over 2 years of runway we believe that that’s going to be enough to get us to profitability. We have the book to business in place that will drive strong revenue growth once we reach that high volume SOP next year. So that gives us a credible way to start growing our revenues and profits to help our reduce our cash spend even more. And so, once again, I understand the source of the question but that’s clearly not the case. We have the most cash and liquidity of any publicly traded LiDAR company and God forbid, if we find ourselves in a scenario where we need more, I have plan A, B, C, D, E, F and many more ways ready to go, you know, always have contingency plans built to put those in place way before you need them.

Is money from Russia plan A or plan F?

The parent company of Forbes magazine is no longer going forward with a sale to billionaire Austin Russell, linked by the media to Russian tycoon and investor Magomed Musaev, Bloomberg reported on Nov. 21.

The Washington Post reported in October that according to obtained audio and video recordings, Kremlin-connected tycoon Musaev claimed he is acquiring Forbes with Russell serving as the "face" of the deal.

While that comment is mostly a joke, Luminar did get $20M in the early days from GVA capital, and it makes you wonder why the CEO is focusing on purchasing Forbes right now. *tin foil hat removed*

Back to the EC...

Joshua Buchalter: And for my follow-up, in the shareholder letter, I think you mentioned you’re on track to achieve a $1 billion of order book growth this year but some of the contracts might slip into next year. Maybe you could elaborate on how much has already been won. I guess how much of that is new versus existing customers and what’s driving, $1 billion was roughly, I believe, what you added last year which, what’s driving, I guess, the bit of a slowdown in the amount of business that you’re signing this year versus last year?

Tom Fennimore: As Josh, look we’re — as we said, in the letter, we’re still on track $1 billion, we do formal tally at end of the year, we kind of don’t it along the way but we already have a few wins in there, some from existing customers, some from new customers. We’ll talk about stuff once our — once our customers are ready to talk about them. So we remain confident that we’re going to get to that billion, we’re sitting here on November 8th, so we have a lot of things already in the year — there’s a few things that we’re hoping to wrap-up here in the few weeks left in the year. Whenever you get to that, there’s always a risk that some things slip, into Q1. But, there’s also a little bit of a cushion in there. So we remain confident in it.

Look, these things that, the longer term opportunity continues to remain and exist. I would say, almost every major automaker is now having serious conversations about implementing, LiDAR technology on their vehicles. It’s a question of when, not if. And the timing of them kind of making these formal awards can be a little lumpy. And so, I wouldn’t read anything in particular to kind of, I would say, an overall, industry slowdown. But I would say, we still remain satisfied with the pace of our commercial activity and discussions, both with new and existing customers.

Winnie Dong: I was wondering if you can provide a current update on the TPK facility ramp in China, where that might stand? And then can you just remind us on the target volume and timeline?

Tom Fennimore: Sure. So, I was actually over in China last week spending some time with the TPK team as well as some other customers over there. I would say that things are proceeding very well so far with TPK. You know, we’re starting, right now for Iris +. We’re making those B samples internally at our Orlando manufacturing facility in some time next year we’ll actually transfer production of the C samples to them. And so, we’re starting to ramp that up, buying the necessary equipment, putting in place the necessary clean rooms. And the TPK team is doing a very good job on that. We’ve been pleased so far with the with the TPK relationship. And, I wouldn’t be surprised if that’s something that continues to expand over time.

With regards to timeline they are planning as I said, start C sample production for us in the first part of next year. And then the plan is to have that facility ready for start production by the end of 2025. The initial capacity that we’re planning that out for is about 600,000 units or LiDARs. And, we also have the ability to grow that as we continue to win more business over there

John Babcock: Okay. And then just one quick follow-up here as it you know pertains to the next-generation LiDAR, how much of that investment has already been made versus how much does still have to be done and then also how where have you made OEMs of this product of capabilities et cetera, has this flowed through into your order book at this point?

Austin Russell: Yes. So I think we’re really just starting to successfully get that off the ground of where we’ve — we spent years’ worth of work on the back end from a technology development standpoint, creating the fundamentals of what’s there, so I would say the — I mean the majority of the time and investment for what’s required to create the fundamentals of the technology for the next gen LiDAR is already done, the real question at this point is being able to progress throughout this coming year to get to a stage of where we can really set this up to be a LiDAR system that can fundamentally be on every vehicle produced and that’s really the goal is that we talk about standardizing and democratizing safety and economy and I think we — we recognize that as fantastic as the products are today, that it’s meant for millions of sensor scale, not tens of millions of sensors in terms of respective scale that we can be able to get out there with and this is exactly what this is designed for so we can really capture the larger automotive industry and also not just the initial vehicle launches that some of these automakers have.

Natalia Winkler: And if I may, we’re just one follow-up on this. How do you guy’s think about ASPs longer term, for China market and outside of China market? And also, like, how should we think about the ASPs that you guys are considering for the order, for the order book, the $1 billion?

Tom Fennimore: Whatever’s in the order book is already have, pricing agreed to with our customers. And so that’s kind of already contractually put in place. Look, we’re always going to get pressure from our — from our customers and automakers, whether they’re in China or globally, to lower our prices. But the one thing that we continue to impress upon with our customers is you got look at the value that our LiDAR provides. And that’s both in terms of the unique technology to enable this next generation ADAS system, as well as highway autonomy. We’ll continue to be able to bring our costs down with our next generation LiDAR but really the value we create in the ecosystem is where we like to focus the conversations on. We tend not to compete on business where it’s who can provide the cheapest costs LiDAR. We like to compete on business where who can provide the best value to the system that our customers are trying to build in.

Austin Russell: And I think it’s also very important to note that and again, this is where obviously the foundation of the business has been a lot but we’ve really been focused on how we continue to monetize the ecosystem around this through our software and AI developments that we’ve had and seen some success with through, for example, these mapping products that we’ve now been able to be out the way through all the different parts of the entire supply chain, even all the way down to the semiconductor level, the LiDAR and how we’ve been able to successfully sell those products even just outside of what we do with the core business. So I think that’s important as part of this, ultimately insurance will play a significant role and I think supporting very significant long-term ASPs associated with safety improvements or the safety improvements will ultimately be king, when it comes to the kinds of value proposition that you can be able to provide.

And this is where we are also — and are successfully launching a new test protocol and system. This is actually Swiss Re is going through an independent third-party test. They’re exclusive insurance partner here to be able to quantify the benefits and safety improvements what the LiDAR can have to be able to basically correlate that into respective insurance savings and costs. And I’ve said, multiple occasions before that the respective savings and value that’s being provided from that alone, from a safety savings standpoint, it’s expected to be significantly more than even just the entire cost of the LiDAR in and of itself. So I think this will be certainly on premium vehicles and even mainstream vehicles. So accidents are expensive. Vehicle collisions are expensive.

Kevin Cassidy: Okay, thanks. Maybe if you could remind us or maybe tell us what the strategy is for expanding your footprint in other models that your current customers say at Volvo and Mercedes and Nissan, how do you get into more models and what would be the timeline for that?

Tom Fennimore: Kevin, we’ve already started to do it at Volvo. We did it at Mercedes. We’ve done it at Polestar. We initially had the 3 and then we went to the 5 earlier this year. And so as you get in with that initial win with the customer and continue to execute, it kind of happens naturally. Now, look, they’re always going to make sure that you’re being honest and competitive on pricing. And so they’ll run RFQs to kind of test the market and keep you honest. But as you execute, as you deliver, as you build the relationship, as they kind of design their software and autonomous systems around you, you execute, you have a real good shot at the next business. That business comes as they renew certain vehicle lines or renew the platforms.

And so the timing of that is more driven by kind of their product launch cycle. But I think you’re going to see us, we’ve done it already and I think you’re going to continue to see us expand our business with our existing customers. And I think the timeline on that’s going to vary depending upon the customer and what their internal timelines are for each of their different products.

11/13/2023 8-K source:

Effective November 13, 2023, Luminar Technologies, Inc. (the “Company”) entered into subscription agreements with Celestica LLC, Phononic, Inc., Scale AI, Inc., Seraph Consulting, Inc., Sinergix, LLC, and Swiss Re Solutions Ltd. (collectively, the “Vendors”) pursuant to which the Company issued to the Vendors 2,201,257, 750,587, 3,537,735, 1,242,138, 377,358 and 503,144 shares of Company Class A common stock, respectively (collectively, the “Shares”), in payment for services rendered or to be rendered under contractual arrangements with the Vendors. Shares issued to the Vendors will vest over time as payments become due and if the Company elects, in its discretion, to make such payments in shares in lieu of cash.

The offering of the Shares issued pursuant to the subscription agreements were registered pursuant to the Company’s shelf registration statement on Form S-3 (File No. 333-262250), which was filed with the Securities and Exchange Commission (the “SEC”) on January 20, 2022, and amended by Amendment No.1 filed with the SEC on February 1, 2022, and which was declared effective by the SEC on February 3, 2022.

A copy of the legal opinion of Orrick, Herrington & Sutcliffe LLP relating to the validity of the Shares is filed with this Current Report on Form 8-K as Exhibit 5.1.

2,201,257 shares to Celestica LLC

750,587 shares to Phononic, Inc.

3,537,735 shares to Scale AI, Inc.

1,242,138 shares to Seraph Consulting, Inc.

377,358 shares to Sinergix LLC

503,144 shares to Swiss Re Solutions Ltd

Luminar has been quite busy executing, high volume facility in Mexico up and running since first half of the year, meeting Volvo's production requirements for SOP. Volvo has started installing Iris sensors into EX90 at Charleston plant, Iris+ sensor B-sample for Mercedes Benz has been delivered, entering C-sample phase at TPK. In Q3 Luminar finished a next generation lidar prototype with live demonstrations to key Automotive OEMs, ultimately being designed for scaling to tens of millions of units where as Iris and Iris+ will likely be produced in the millions. Iris and Iris+ sensors are currently on the higher end of cost but the next generation lidar is targeted for lower BOM (if they can reach economies of scale, an advantage most 905nm based systems already have due to commodity grade lasers and photodetectors), Luminar expects to maintain high profit margins by providing additional value outside just the sensor and perception software, eg: mapping, insurance, whether this fits well with Auto OEM's own offerings or competes is unknown. Q3 operating cash flow $(56.5)M, free cash flow $(60.8)M, they believe they'll end 2023 with >$300M in cash, cash equivalents, and marketable securities, and aiming to increase free cash flow by Q4 and into 2024 as they incur less one time costs associated with product launches.

Valeo

Scala 2 currently in MB S-Class, next generation Scala 3 offers increased resolution and range, as well as perception and AI for highway speed applications. Scala 3 has already been chosen by a leading Asian manufacturer and a leading American robotaxi company with combined orders worth over $1B euros, its also won CES 2024 Innovation award, at CES 2024 they'll be offering more details around their AI based perception software.

Mobileye

Q2 EC, Amnon Shashua (CEO) states "The FMCW LiDAR is on track for second generation LiDARs around 2027/2028 timeframe where we feel that first generation autonomous vehicles would be served with final flight LiDARs and second generation with FMCW." Looks like they're continuing to use Luminar lidar until they finish their FMCW based lidar, source.

In Q3 EC no update on Luminar partnership or internal lidar development.

China

As most things in life it only takes so long before things become political.

In August Congressional Research Service (CRS) released the article: U.S.-China Competition in Emerging Technologies: LiDAR which claims China based Lidar companies have an unfair advantage by China's industrial policies and lack of IP enforcement, and since Lidar plays a dual role for both civilian and military use this may pose a threat to both economic competitiveness in the U.S. and national security. The top two Chinese based lidar companies both have ties to the military, Hesai with China Electronics Technology Group Corporation and Robosense with Harbin Institute of Technology.

In November members of the House Select Committee on Strategic Competition between the United States and the Chinese Communist Party (CCP) call for an investigation into whether Chinese based lidar company technology should be placed on Defense Department’s Chinese Military Companies List, Commerce’s Bureau of Industry and Security Entity List, and Treasury’s Non-SDN Chinese Military-Industrial Complex Companies List, for same reasons as earlier stated, source.

Regardless of the politics both Robosense and Hesai have been busy producing at scale...

Robosense

In February announced partnership with Toyota to supply their RS-Lidar-M series:

By equipping them with the RS-LiDAR-M series LiDAR ("M-series" for short), RoboSense will empower Toyota models with accurate perception capabilities, guard the driving safety of Toyota's intelligent models, and promote the series production and large-scale application of LiDAR in the automotive industry. The M-series is a featured automotive-grade, revolutionary product from RoboSense for vehicle series production. It is the only second-generation smart solid-state LiDAR in the world to achieve the automotive-grade series production. It adopts a revolutionary chip-based 2D scanning solution, which boasts supreme performance and reliability. At present, the M-series has obtained nominated orders for more than 50 models from nearly 20 car companies, including Toyota, with an expected order volume of more than 10 million units.

In Q3 achieved record sales volume of ~60,000 units, for the year 2023 over 106k sensors sold which surpassed their cumulative sales for 2020-2022 (~94k sensors).

In October 2023, RoboSense increased its automotive OEM model design wins from 58 to 61. During the same period, RoboSense worked with 11 OEMs and Tier 1 customers to achieve mass production for 19 vehicle models integrating the company’s LiDAR, marking substantial growth compared to June 2023's nine clients and 13 mass-produced models. As the automotive industry continues to develop cutting-edge perception systems to create more intelligent vehicles and meet customer demand for advanced driver assistance systems, RoboSense has experienced rapid growth.

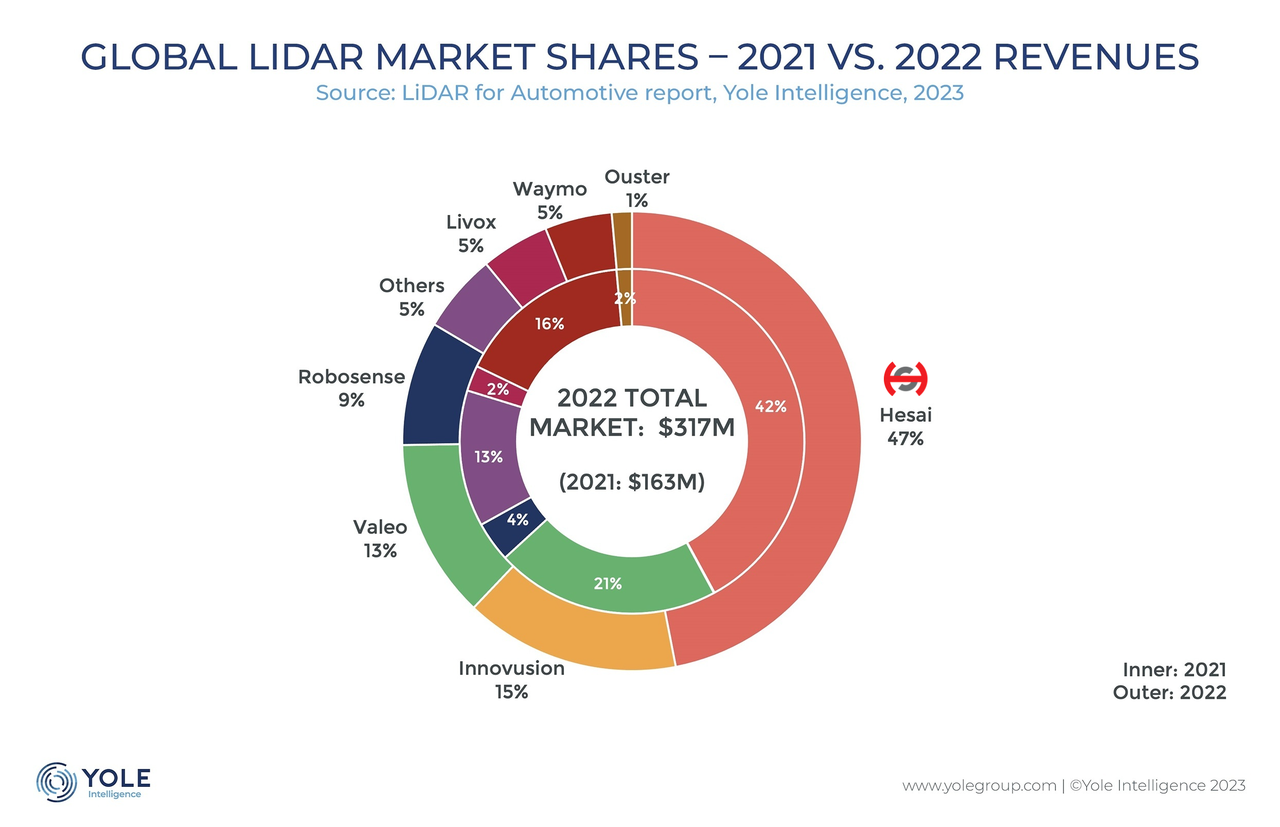

Hesai

Yole Intelligence report for 2023 names Hesai as #1 automotive lidar supplier with largest market share by revenue:

- Polestone 01, a full-size luxury SUV model was officially released on August 22. Its powerful intelligent driving system features a long-range lidar - AT128, and two blind-spot fully solid-state lidars - FT120. The combination of three lidars covers a horizontal FOV of 280°, providing ultra-high resolution 3D perception capability. Polestone 01 is also the world's first series-production vehicle model to feature fully solid-state lidars source

- Hesai’s AT128 lidar will be at the core of the Human Horizons HiPhi Z’s Advanced Driver Assistance Systems (ADAS). The luxury electric vehicle is now available for sale in Germany and Norway source

- design win with FAW Group, one of the largest automotive OEMs in China, for their next generation EV model under Hongqi brand. It marks the first series production design win for Hesai's ultra-thin long-range lidar ET25. The program is expected to begin mass production and delivery by the first half of 2025 source

- design win with Neta Auto's new series production vehicle. Hesai will supply ultra-high resolution long range lidar AT128 for Neta Auto's upcoming vehicle model which is expected to launch in the first half of 2025 source

- design win with leading Chinese electric vehicle maker Leapmotor. Hesai will supply ultra-high resolution long range lidar AT128 for Leapmotor's upcoming series production vehicle model source

- design win with Great Wall Motors, Multiple passenger vehicle models from GWM will be equipped with Hesai's ultra-high resolution long range lidar AT128, with plans for mass production and delivery starting in 2024 source

Also wins CES 2024 Innovation Award for ET25 ultra-thin long range sensor

Summary

In short many publicly traded lidar companies have been claiming big RFQs coming to close and nominations announced end of year, so far it's still crickets, much of 8-Ks released are still loosely worded around partnerships, forward-looking order books (which to be fair may be all suppliers get when working with Auto OEMs, most consumers don't know or care if their vehicle is equipped with Bosch electronic power steering or Valeo 79GHz Radar for blind spot detection), and rollouts on expensive vehicle models.

I have some skepticism around Auto OEMs ability to code and scale for ADAS features so I expect more marketing and differentiation between sensor suppliers to be based on perception features going into 2024 and 2025, basically anything that makes the OEM's life easier and doesn't directly compete with the experience they wish to provide to consumers.

While the Automotive OEMs cautiously decide their next steps the lidar space prepares for additional consolidation, raising money at let's say not the greatest time, executing new retention agreements for keeping upper management, and competing with China. Earlier in the year leaders in the industry made comments around only a handful of lidar companies to survive in the end, call it 3-5 for automotive.

So as an update from 2023 being the year of slogging through RFQs, 2024 should hopefully be the year of announcing RFQ wins and share price appreciations--for the lucky.

Full disclosure: I'm still speculating on Microvision to emerge as one of the leaders due to their carry over expertise in LBS from heads up displays and AR, cost effective approach with 905nm based system (OEMs are cheap), and their acquisition of Ibeo allowing them to provide perception features sooner than the competition.

This is not financial advice.